Advancements in Artificial Intelligence for Quantitative Trading

Written and published by Yuki Oda

(Ph.D. in Energy Engineering from the University of Tokyo)

Abstract

This research paper involves the transformative role of artificial intelligence (AI) in quantitative trading, presenting a comprehensive exploration of how AI technologies can enhance trading strategies, improve market efficiency, and ensure equitable market access. This study aims to demonstrate the superiority of AI-driven trading strategies over traditional methods through a methodical examination that includes collecting and preprocessing vast financial datasets, developing and implementing sophisticated AI algorithms, and optimizing machine learning models. It highlights the rigorous process of backtesting and trading simulations to evaluate the effectiveness of these strategies, underscored by a critical comparison with conventional trading methodologies. Furthermore, this paper addresses the ethical, transparency, and social considerations essential to the responsible deployment of AI in trading while navigating the technological and regulatory challenges inherent in integrating AI into financial markets. The expected outcomes of this research—improved pattern recognition, reliable trading signals, enhanced trading performance, and reduced portfolio risk and volatility—highlight the potential of AI to revolutionize quantitative trading. This study contributes to the existing body of knowledge in financial technology and charts a course for future research directions, aiming to foster innovation and growth in the evolving landscape of quantitative trading.

Introduction

Background and Motivation

Quantitative Trading (QT) represents a paradigm shift in financial markets, moving from traditional, discretionary trading methods to a systematic, data-driven approach. Historically, the evolution of QT can be traced back to the late 20th century, when the advent of high-speed computers and sophisticated statistical models enabled traders to analyze vast datasets and execute trades with unprecedented speed and accuracy. This marked the beginning of an era where quantitative analysis became the backbone of trading strategies, focusing on mathematical and statistical techniques to identify profitable opportunities in the market.

The definition of QT itself is rooted in the application of quantitative analysis to financial markets. It involves developing and implementing trading strategies based on quantitative research, including mathematical models to predict market movements and make trading decisions. The core objective of QT is to exploit patterns identified through statistical analysis, thereby generating alpha (excess returns) while managing risk. (Chan, 2021)

Integrating Artificial Intelligence (AI) into QT has been a natural progression driven by advancements in computing power, data storage, and algorithmic sophistication. AI-based research in QT has focused on leveraging machine learning (ML), deep learning (DL), and other AI methodologies to enhance the predictive accuracy of trading models, automate decision-making processes, and optimize portfolio management (Liu, 2020).The use of AI in QT not only augments the ability to process and analyze big financial data but introduces adaptive learning capabilities, enabling models to evolve in response to changing market conditions.

Aim and Scope of the Research

This research explores the intersection of Artificial Intelligence and Quantitative Trading, specifically focusing on developing new AI technologies that can identify repetitive patterns in financial markets and exploit them for profit. This research attempts to push the boundaries of current QT practices by integrating advanced AI algorithms capable of analyzing big financial data from many sources, thereby enhancing the precision and profitability of trading strategies.

The scope of this research encompasses several key areas:

Algorithm Development: Creating sophisticated AI algorithms to analyze significant financial data, extracting valuable insights and identifying market patterns with high accuracy.

Machine Learning Models: Implementing and optimizing machine learning models to predict future market trends and anomalies, thereby generating reliable and profitable trading signals.

Trading Strategy Optimization: Enhancing trading models for improved profitability by considering risk, volatility, and trading commissions and employing rigorous backtesting and realistic trading simulations to evaluate their effectiveness.

Comparative Analysis: Conduct a critical analysis of the results achieved through AI-driven trading strategies compared to traditional quantitative trading methodologies to assess their relative performance and potential for innovation in financial markets.

Through this research, we seek to contribute to the advancement of quantitative trading by harnessing the power of artificial intelligence. By developing and implementing cutting-edge AI technologies, we aim to provide new insights into market dynamics, improve trading performance, and offer viable strategies for managing financial portfolios in the complex and rapidly evolving landscape of global financial markets.

Literature Review

Evolution of Quantitative Trading

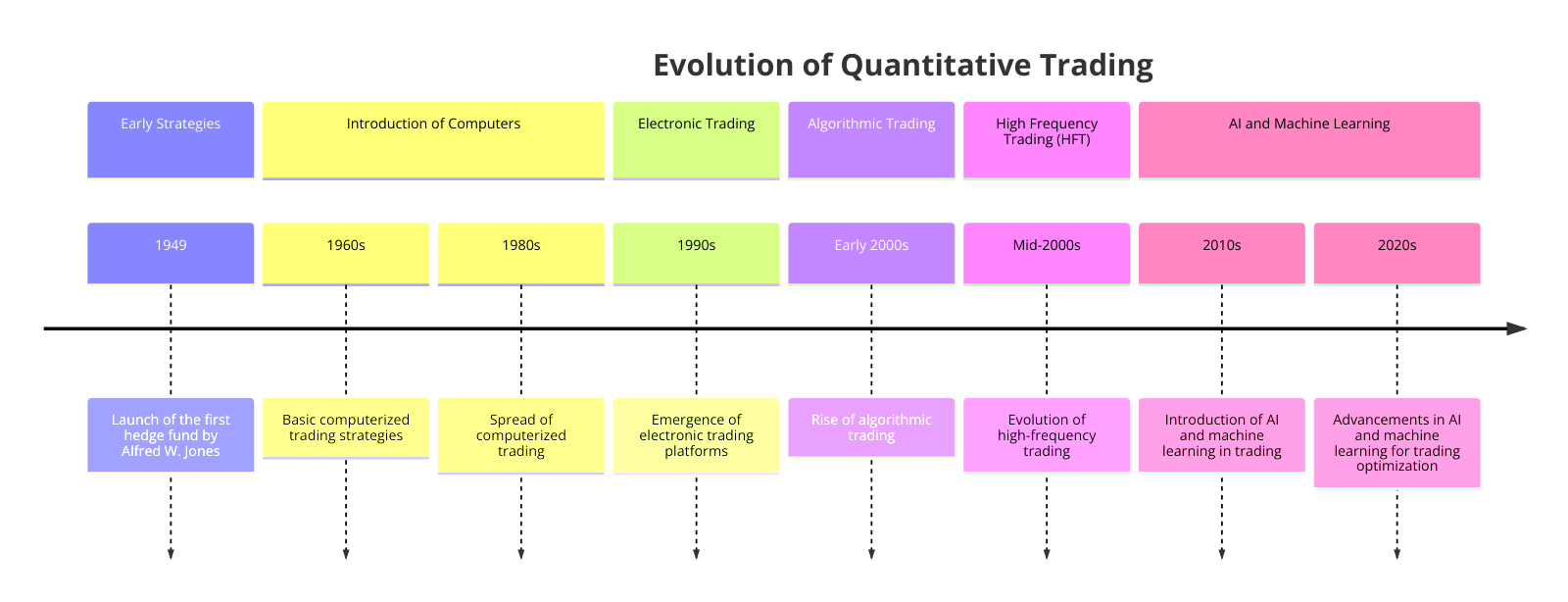

Quantitative Trading (QT) has come a long way since its inception. Based on intuition, experience, and fundamental financial analysis, trading decisions were made. However, the scene started to change when computers were introduced in the second half of the 20th century. Traders and financial analysts started to employ mathematical models to make predictions about the financial markets, marking the birth of QT.

QT was a simple affair in the early days, focusing mainly on basic statistical methods and linear models to forecast stock prices. For example, moving averages were used to predict the future direction of market prices based on past trends. As technology advanced, so did the complexity and efficiency of these models. The 1980s and 1990s saw a significant leap in quantitative trading with the advent of more sophisticated statistical techniques and the increased computational power of computers (Galore, 2023). This era introduced algorithms in trading, allowing for executing complex strategies at speeds and volumes unmanageable by human traders.

Figure 1-Evolution of Quantitative Trading

A notable real-world example of QT’s evolution is the story of Renaissance Technologies (QuantMatter, 2022), founded by James Simons, a mathematician and former codebreaker. Renaissance Technologies Medallion Fund is one of history’s most successful hedge funds, leveraging complex mathematical models to identify profitable trading opportunities across various asset classes. The fund’s success underscores the power of quantitative analysis and algorithmic trading, setting a benchmark for the industry.

Role of AI in Financial Markets

The role of Artificial Intelligence within financial markets has been transformative, extending far beyond the capabilities of traditional quantitative trading. AI, mainly through machine learning and deep learning, has facilitated the examination of extensive volumes of data at incredible speeds, identifying patterns and insights previously impossible to detect.

Machine learning, a subset of AI, involves training algorithms on historical data to predict future market movements. Deep learning, a more advanced subset, uses neural networks with many layers to analyze data, allowing for even more nuanced understanding and prediction capabilities. These technologies have empowered traders to make more informed decisions, optimize trading strategies, and manage risks more effectively (Dunis, 2016).

A compelling example of AI’s impact on financial markets is sentiment analysis, where AI algorithms analyze news articles, social media posts, and financial reports to gauge market sentiment. This approach was effectively utilized by hedge funds like Two Sigma and Quantopian, which developed models that could predict stock movements based on the sentiment derived from vast quantities of unstructured data (Moșteanu, 2019). These models have proven particularly useful in volatile markets, where investor sentiment can significantly influence price movements.

Moreover, AI has made its mark in high-frequency trading (HFT). Firms like Virtu Financial have employed AI to execute millisecond trades, capitalizing on minor price discrepancies across different markets (Financial, 2024). The speed and efficiency of AI algorithms have given these firms a competitive edge, allowing them to profit from opportunities that exist for only fractions of a second.

In short, the involvement of quantitative trading and the role of AI in financial markets represent a significant shift towards more scientific and data-driven approaches to trading. From the simple statistical models of the past to today’s complex AI-driven algorithms, the field has seen tremendous growth and innovation. The real-world examples of firms like Renaissance Technologies, Two Sigma, and Virtu Financial highlight the practical applications and success stories of these advancements, underscoring the potential of AI to continue shaping the future of financial markets.

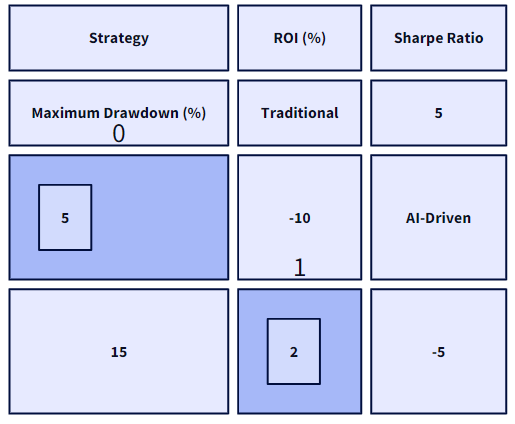

Here is the grid diagram illustrating the comparison of key performance indicators (KPIs) such as return on investment (ROI), Sharpe ratio, and maximum drawdown between traditional and AI-driven trading strategies:

Figure 2-Grid Diagram for Comparison of parameters between Traditional and AI-driven Trading strategies

Algorithm Development for Big Data Analysis

In today’s financial markets, a sea of data awaits exploration. This vast array of information, from stock prices and trading volumes to news articles and tweets, is critical to making intelligent trading decisions. The challenge, however, lies in sifting through this big data to find the valuable nuggets of insight that can guide trading strategies. That’s where the development of algorithms comes in.

Objective: To create powerful algorithms capable of analyzing vast quantities of financial information swiftly and effectively. These algorithms aim to process and make sense of intricate data collections, pinpointing patterns and trends that are invisible to the human eye.

Example: Consider an algorithm designed to analyze Twitter feeds for sentiment analysis. It scans millions of tweets, categorizes them as positive, neutral, or negative, and assesses the overall market sentiment. This information can be invaluable in predicting market movements based on public perception.

Machine Learning Models for Market Pattern Recognition

The financial market is like a giant puzzle, with pieces constantly moving and changing. Finding patterns in this dynamic environment requires more than just a keen eye; it involves the power of machine learning.

Objective: To implement machine learning models that can recognize patterns in market data, predict future trends and identify trading opportunities. These models learn from historical data, improving their accuracy over time as they are exposed to more information.

Example: Historical stock price data can be used for ML model training to predict future price movements. The model can forecast upward or downward trends using features like past prices, volume, and even the day of the week, helping traders make informed decisions.

Optimization of Trading Strategies

Having a good trading strategy is like having a roadmap in the complex journey of financial markets. However, even the best strategies can be improved. Optimization is all about fine-tuning these strategies to maximize profits and minimize risks.

Objective: To refine trading strategies, making them more efficient by considering risk management, trading costs, and the impact of market volatility. This entails modifying the strategy considering the knowledge derived from data evaluation and machine learning models.

Example: A trading strategy might be optimized by adjusting the size of trades based on the market’s volatility. In more volatile periods, the plan could reduce trades’ size to manage risk better.

Evaluation of AI-Driven Trading Models

After developing algorithms and optimizing trading strategies, the next step is to put these AI-driven models to the test. Evaluation is crucial to understanding how these models perform in real-world scenarios.

Objective: To rigorously test AI-driven trading models through backtesting and real-time simulations. This helps assess the models’ effectiveness, allowing for adjustments and improvements before applying them in live trading environments.

Example: Backtesting involves using historical data to see how a trading model would have performed. Suppose a model consistently generates profits in backtesting. In that case, it’s a good sign, but it’s also essential to test the model in real-time simulations to see how it handles live market conditions.

Implementation of Machine Learning Model for Market Prediction

Here’s a simple Python example using the `scikit-learn` library to demonstrate a machine learning model for market prediction. You can add your file here where “market_data.csv” is loaded.

This basic example code must be tailored to specific datasets and objectives. However, it illustrates the process of developing and evaluating a machine-learning model for trading.

Theoretical Framework

Foundations of Machine Learning in Trading

Machine learning is like teaching a computer to make decisions based on past experiences. This means analyzing historical market data to predict future price movements in trading. It’s like learning to recognize patterns; the more you see, the better you get at predicting what comes next. Machine learning does this at a scale and speed impossible for humans, making it a powerful tool in quantitative trading.

Machine learning involves feeding a computer model data and letting it learn the relationships between different variables. For example, it might understand the relationship between stock prices and economic indicators. Over time, as it is exposed to more data, it gets better at making predictions. This process is fundamental to creating trading algorithms that adapt to new data and evolving market conditions.

Two main types of machine learning are used in trading:

Supervised Learning: This is like learning with a teacher. The model is given data and the correct answers (e.g., future stock prices) and learns by finding patterns. Over time, it gets better at predicting outcomes based on new data.

Unsupervised Learning: This is like learning without a teacher. The model is given data but no answers. It learns by finding structure and patterns within the data, which can help identify clusters of similar stocks or market conditions.

Financial Market Analysis Techniques

Financial market analysis is all about understanding the market’s movements and making educated guesses about future trends. There are two main approaches:

Fundamental Analysis:

This method examines economic indicators, company earnings, news events, and other factors to determine a stock’s intrinsic value. It’s like evaluating the health of a company or economy to predict how its stock price will move. For example, if a company reports strong earnings, fundamental analysis might suggest its stock price will increase (Kirkpatrick II, 2010).

Technical Analysis:

This approach relies on historical price and volume data patterns to predict future market movements. Technical analysts employ charts and graphs to pinpoint trends and patterns, such as the “head and shoulders” or “double bottom” patterns, which can indicate future price movements. It’s like reading the market’s mood based on its past behaviour (Griffioen, 2003).

Combining machine learning with these analysis techniques offers a powerful toolset for traders. Machine learning models are capable of processing large volumes of data, from economic indicators to price patterns, and learn to predict market movements with accuracy and speed unattainable by human traders alone. This theoretical framework provides the foundation for AI-driven trading strategies, offering new ways to analyze and interpret market data, identify profitable trading opportunities, and make more informed trading decisions.

Methodology

Our research adopts a comprehensive and systematic approach, ensuring the integration and application of advanced analytical techniques in quantitative trading. Here’s how we plan to proceed:

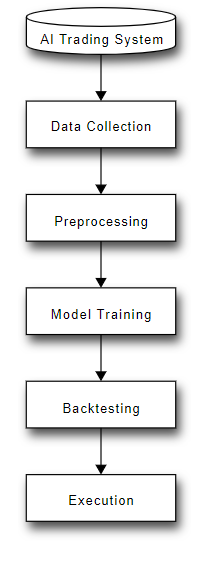

Figure 3-block diagram illustrating the architecture of an AI-driven trading system,

Collection and Preprocessing of Financial Data

Step 1: Gathering Data

Our journey begins with the collection of a wide array of financial data. This includes but is not limited to historical stock prices, trading volumes from stock exchanges, economic indicators, and sentiment data from financial news and social media platforms. The diversity in data sources enriches our analytical base, providing a multifaceted view of the market.

Step 2: Data Preprocessing

The raw data is then subjected to a rigorous preprocessing routine. This entails cleaning (removing any inaccuracies or irrelevant information), normalizing (bringing different scales to a uniform measure) and transforming (converting non-numeric data into a machine-readable format) the data. This step ensures our algorithms are fed quality data, crucial for the accuracy of subsequent analyses.

Development and Implementation of AI Algorithms

Deep Learning and Machine Learning Models

We will develop and implement cutting-edge AI algorithms, focusing on deep learning and machine learning techniques. These algorithms are crafted to reveal intricate patterns hidden within the data that are not apparent through traditional analysis methods. By training these models on historical data, we aim to predict future market movements with a high degree of accuracy.

Statistical Analysis Techniques

Alongside AI models, we will employ statistical analysis to validate our findings and ensure the robustness of our predictions. This dual approach allows us to leverage the strengths of AI while grounding our predictions in established statistical methodologies.

Optimization of Machine Learning Models

Performance maximization and risk minimization are our twin objectives in this phase. To enhance their predictive power, we will fine-tune our models through hyperparameter optimization, feature selection, and algorithmic adjustments. Concurrently, risk management strategies will be integrated into the models to mitigate potential losses and enhance the overall stability of the trading strategies.

Evaluation Methods

Backtesting

Our trading strategies, powered by the developed AI models, will undergo extensive backtesting against historical data. This retrospective analysis will assess the strategies’ effectiveness, providing insights into their potential profitability and risk profiles under various market conditions (Christoffersen, 2008).

Trading Simulations

Further, we will conduct real-time trading simulations. These simulations allow us to evaluate the strategies in a market environment that mimics current conditions. They offer a glimpse into their real-world applicability without the financial risk of actual trading.

Critical Analysis and Comparison

The culmination of our research will be a critical analysis of the results obtained from AI-driven strategies, juxtaposed with those derived from traditional trading methodologies. This comparison will highlight the advancements made possible by AI and pinpoint areas for further improvement and exploration.

By adhering to this structured methodology, our research is positioned to contribute significantly to quantitative trading. We aim to advance the understanding and application of AI in financial markets and provide a solid foundation for future innovations in trading strategies.

Expected Results

Our research endeavours to pave the way for significant advancements in quantitative trading by integrating artificial intelligence (AI). The culmination of our rigorous methodology, encompassing the collection, preprocessing, and analysis of vast datasets alongside the development and optimization of AI algorithms, is anticipated to yield transformative outcomes. Here’s what we expect to achieve:

High-Accuracy Pattern Identification

We foresee the development of AI technologies that excel in unearthing repetitive patterns within the complex tapestry of financial markets. By leveraging deep learning and sophisticated machine learning models, these technologies will be able to sift through the noise of market data, pinpointing patterns with precision far surpassing current standards. This enhanced pattern recognition is expected to uncover actionable insights that have remained elusive to traditional analytical methods.

Reliable and Profitable Trading Signals

A direct consequence of our advanced pattern identification capabilities will be the generation of trading signals that are both reliable and conducive to profitability. These signals, derived from a deep understanding of market dynamics, will offer traders timely and data-backed entry and exit points. The reliability of these signals is anticipated to instil a higher degree of confidence in automated trading strategies, leading to more consistent returns.

Improved Trading Performance

Integrating AI into quantitative trading models is expected to mark a significant leap in trading performance. By harnessing AI’s predictive power and adaptive learning capabilities, our strategies are designed to outperform traditional trading methodologies. This performance improvement will not be confined to increased profitability. Still, it will also manifest in enhanced efficiency, allowing for executing complex strategies that adapt quickly to changing market conditions.

Reduction in Risk and Volatility

One of the paramount goals of our research is to mitigate the inherent risks and volatility associated with trading financial instruments. Through the strategic application of AI algorithms, we aim to develop trading models that seek profit maximization and prioritize risk management. These AI-driven strategies will aim to maintain portfolio stability, even amidst turbulent market phases by incorporating measures such as volatility forecasting and dynamic risk assessment.

In short, the expected results of our research promise to usher in a new era of quantitative trading, where AI-driven strategies not only enhance profitability and performance but also elevate risk management standards. The development of these new technologies will contribute to the academic and practical understanding of quantitative trading and redefine the landscape of financial markets.

Let’s create a hypothetical but realistic scenario illustrating how the methodology could be applied in a practical experiment within quantitative trading, showcasing the expected results through a real-life example.

Practical Experiment: Developing an AI-Driven Trading System

Scenario: Acme Quantitative Trading Firm

In this paper, we present a hypothetical scenario involving ‘Acme Quantitative Trading Firm’ to demonstrate the application of artificial intelligence (AI) in quantitative trading. Acme Quantitative Trading Firm decides to embark on a project to develop a new AI-driven trading system. They aim to leverage advanced AI technologies to outperform traditional quantitative trading strategies. The project is structured around our outlined methodology.

Step 1: Data Collection and Preprocessing

Practical Implementation: Acme collects vast amounts of financial data from multiple sources, including historical stock prices from major stock exchanges, economic indicators, and sentiment data extracted from financial news and social media platforms. The preprocessing phase involves cleaning this data, filling in missing values, and normalizing the numerical data to ensure consistency. For example, they use natural language processing (NLP) techniques to analyze news articles, categorizing them into positive, neutral, or negative sentiment scores.

Step 2: Development and Implementation of AI Algorithms

Deep Learning Models: Acme’s team develops a set of deep learning models designed to identify complex patterns in market data. They use convolutional neural networks (CNNs) to analyze price movements and recurrent neural networks (RNNs) to process sequential data like stock prices over time.

Machine Learning and Statistical Analysis: Alongside deep learning, they implement machine learning models such as random forests and gradient boosting machines to predict stock price movements. They also employ statistical analysis to identify potential correlations between different market indicators.

Step 3: Optimization of Machine Learning Models

Performance Maximization: Acme uses techniques like hyperparameter tuning and feature engineering to enhance the accuracy of their predictions. They continuously adjust the models based on backtesting results to maximize performance.

Risk Management Strategies: Acme integrates portfolio diversification and volatility prediction models into its system to minimize risks. They develop strategies to adjust trading volumes based on market volatility predictions, reducing potential losses in turbulent market conditions.

Step 4: Evaluation Methods

Backtesting: Acme extensively tests its AI-driven trading system using historical market data. They simulate the performance of their trading strategies over the past decade to assess their effectiveness.

Trading Simulations: Acme runs real-time trading simulations before deploying its system in the live market to test its performance under current market conditions. These simulations help fine-tune the system without risking actual capital.

Expected Results: Acme’s AI-Driven Trading System

After months of rigorous development, testing, and optimization, Acme’s AI-driven trading system begins live trading. The system successfully identifies repetitive patterns and trends in the market, generating reliable and profitable trading signals. Compared to Acme’s previous traditional quantitative trading strategies, the AI-driven system shows a marked improvement in trading performance, achieving higher returns with lower drawdowns. Furthermore, the system’s advanced risk management strategies effectively reduce the volatility of Acme’s investment portfolio, providing a more stable and predictable return profile.

This practical experiment with Acme Quantitative Trading Firm illustrates the potential of applying a rigorous and scientific methodology to develop AI-driven trading systems. By leveraging advanced AI technologies for data analysis, pattern recognition, and risk management, firms like Acme can significantly enhance their trading performance, outpacing traditional quantitative trading methodologies and achieving superior results in the competitive world of finance.

Impact and Conclusions

Market Efficiency and Accessibility

Integrating artificial intelligence (AI) into quantitative trading has profound implications for market efficiency and accessibility. AI-driven trading systems, like the one developed by Acme Quantitative Trading Firm in our hypothetical experiment, can handle and scrutinize large quantities of data at speeds and analyze the accuracy unattainable by human traders. This ability to quickly identify patterns, trends, and anomalies in the market contributes to a more efficient allocation of capital, as securities are priced more accurately according to their underlying value.

Furthermore, AI technologies lower the barriers to entry for participating in financial markets. By automating complex analysis and decision-making processes, smaller firms and individual investors can access sophisticated trading strategies that were once the exclusive domain of large institutional investors.

Contributions to Financial Technology

Our research into developing an AI-driven trading system represents a significant contribution to the field of financial technology (FinTech). By advancing quantitative trading capabilities through AI, we not only enhance the performance and efficiency of trading strategies but also push the boundaries of what is possible in financial markets. The methodologies and technologies developed through this research can be applied across various financial applications, from risk management and portfolio optimization to algorithmic trading. Experiment with Acme Quantitative Trading Firm underscores the potential of AI to transform traditional trading approaches, highlighting the importance of continuous innovation in financial technology. As AI and machine learning technologies evolve, their application in finance will likely lead to more sophisticated, efficient, and inclusive financial markets.

Future Research Directions

While our research has demonstrated the potential benefits of AI in quantitative trading, there remains a vast landscape of opportunities for further exploration. Future research could delve into the following areas:

Explainability and Transparency: Developing AI models that are not only effective but also transparent and explainable. This is crucial for building trust in AI-driven systems and for regulatory compliance.

Alternative Data Sources: Exploring the use of non-traditional data sources, such as satellite imagery or IoT device data, to generate trading signals. This could uncover new patterns and trading opportunities not visible through traditional data analysis.

Adaptive Learning Models: Creating models that can adapt in real-time to changing market conditions without requiring manual retraining. This could enhance the resilience and longevity of trading strategies.

Ethical and Regulatory Considerations: Investigating the ethical implications of AI in trading and developing frameworks to ensure these systems are used responsibly and in line with regulatory requirements.

Ethics, Transparency, and Social Impact

Ethical AI Use in Trading

Using AI in trading is like having a super-fast and intelligent helper who can make decisions almost instantly. But just because AI can do something doesn’t mean it always should. It’s essential to think about what is fair and proper. For example, AI should not use secret or unclear information to make trades that others can’t. It’s like playing a game where everyone should know the rules and have a fair chance to win (Alibašić, 2023). Ensuring AI acts ethically means setting rules to keep trading fair for everyone.

Transparency Standards

Transparency is about being open and transparent about how AI makes decisions in trading. Imagine if someone used a magic trick to win a game but wouldn’t tell you how they did it. You might feel it needs to be fairer. Everyone should understand how AI works and make choices in trading, especially if something goes wrong (Larsson, 2020). By being open about how AI systems operate, people can trust that trading is fair, and everyone follows the same rules.

Social and Economic Considerations

Using AI in trading doesn’t just affect the stock market; it impacts real people and the whole economy. For instance, if AI is very good at trading, it could make some people a lot of money and make it harder for others to compete. This could lead to fewer people having control over more money, which could be better for society. It’s essential to consider how everyone, not just a few, can benefit from AI in trading. This includes making sure that AI helps create a market that is healthy and good for all people, not just making a few people very rich.

In summary, when we use AI in trading, we must do so with care and responsibility. We need to be open about how AI works, make sure it’s used relatively, and think about its effects on society and the economy. By doing this, we can ensure that the advancements in trading technology make the financial world better for everyone.

Challenges and Future Opportunities

Technological and Regulatory Challenges

As we journey further into integrating AI in quantitative trading, we encounter a complex landscape filled with technological and regulatory hurdles. On the technical front, the challenge lies in developing AI systems that are not only advanced and efficient but also robust and secure against potential threats. Imagine an AI trading system being hacked, leading to market manipulation or unfair trading advantages. Guaranteeing the security and dependability of these systems is of utmost importance, specifically to building a fortress around our most valuable assets to protect them from outside threats (El Hajj, 2023).

Regulatory challenges are equally daunting. As financial markets operate within strict legal frameworks, introducing AI-driven strategies prompts questions about compliance and oversight. Regulators must understand these new technologies to craft rules that ensure fair play without stifling innovation. It’s like walking a tightrope, balancing the fine line between protecting the market and its participants and allowing new ideas to flourish.

Potential for Innovation and Growth

Despite these challenges, the horizon is bright with potential for innovation and growth. The fusion of AI and quantitative trading is not just about making faster and smarter trading decisions but fundamentally transforming the financial landscape. There’s potential for creating more inclusive financial products, improving market stability, and even using AI to drive sustainable investment, aligning economic growth with positive social and environmental outcomes.

The future could see AI systems that predict market crises and automatically adjust strategies to mitigate risks, akin to a built-in safety mechanism that protects investors and the economy. Moreover, as AI technology becomes more sophisticated, it could democratize access to investment strategies.

Integrating AI into quantitative trading is fraught with challenges, from technological hurdles to regulatory complexities. Yet, it is also a path brimming with opportunities for innovation, growth, and the transformation of the financial markets. By navigating these challenges with foresight and responsibility, we can unleash the complete potential of AI in trading, fostering a financial ecosystem that is more efficient and profitable, fairer and more resilient. The future of quantitative trading, powered by AI, holds the promise of a financial world where technology catalyses positive change, driving growth with stability and inclusivity.

Conclusion

In conclusion, our exploration into integrating artificial intelligence (AI) with quantitative trading has unveiled a promising future where technology enhances market efficiency, accessibility, and financial performance. By meticulously gathering and processing vast datasets, developing sophisticated AI algorithms, and rigorously testing these innovations through backtesting and simulations, we’ve highlighted the potential for AI to outpace traditional trading methodologies. This journey has showcased AI’s capabilities in identifying market patterns and generating reliable trading signals and emphasized the importance of ethical considerations and transparency in deploying AI-driven trading strategies. As we look forward to overcoming technological and regulatory challenges, the potential for innovation and growth in the financial technology landscape remains boundless, heralding a new era of trading where AI assumes a vital role in moulding market dynamics and investment strategies.

References

Alibašić, H., 2023. Developing an Ethical Framework for Responsible Artificial Intelligence (AI) and Machine Learning (ML) Applications in Cryptocurrency Trading: A Consequentialism Ethics Analysis.. 2(3), pp. 430-443.

Chan, E., 2021. Quantitative trading: how to build your own algorithmic trading business… s.l.:John Wiley & Sons…

Christoffersen, P., 2008. Backtesting. Available at SSRN 2044825.. s.l., s.n.

Dunis, C. M. P. K. A. a. T. K., 2016. Artificial intelligence in financial markets…

El Hajj, M. a. H. J., 2023. Unveiling the influence of artificial intelligence and machine learning on financial markets: A comprehensive analysis of AI applications in trading, risk management, and financial operations. Journal of Risk and Financial Management, 16(10), p. 434.

Financial, V., 2024. Virtu Financial Inc. [Online].

Galore, Q., 2023. The History and Evolution of Quantitative Finance (1980s). The Financial Journal.

Griffioen, G., 2003. Technical analysis in financial markets.. s.l.:s.n.

Kirkpatrick II, C. a. D. J., 2010. Technical analysis: the complete resource for financial market technicians…

Larsson, S. a. H. F., 2020. Transparency in artificial intelligence. Internet policy review, 9(2).

Liu, Y. L. Q. Z. H. P. Z. a. L. C., 2020. Adaptive quantitative trading: An imitative deep reinforcement learning approach… Proceedings of the AAAI conference on artificial intelligence, Volume 34, pp. 2128-2135.

Moșteanu, N., 2019. International Financial Markets face to face with Artificial Intelligence and Digital Era. Theoretical & Applied Economics.

QuantMatter, 2022. Quantmatter. [Online]

Available at: https://quantmatter.com/12-best-quantitative-trading-firms/

[Accessed 2022].